March 2, 2026

If you work in tech, it is common for RSUs to become the largest part of your balance sheet before you realize it. In the startup world especially, we often see a familiar scenario. Someone joins a fast-growing company, the equity grants look promising, the valuation keeps climbing, and there never seems to be a reason to rush into a formal plan. Everything feels stable, and the future feels predictable.

Then the industry does what it always does. Markets shift, valuations reprice, headlines turn, and what once felt like steady growth becomes a rapid decline in paper wealth. It happens quickly, and it catches even the most financially savvy professionals off guard.

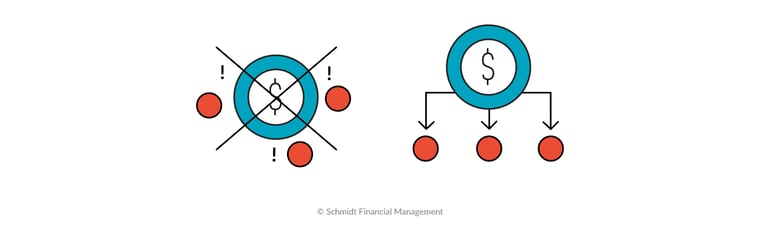

This is the reality of concentrated wealth in a volatile industry. When one company drives both your income and your investment exposure, your financial life can move in the same direction as the tech cycle itself.

The goal here isn’t to sell everything and miss potential upside. It’s to shift enough of your RSU exposure so that your future isn’t overly dependent on one stock, one CEO, or one market cycle. Diversification helps separate your long-term financial stability from the natural swings of the tech world so your future is supported by more than one company’s trajectory.

Common Triggers for RSU Diversification

Most executives already know when it is time to diversify. These are a few natural moments to take action:

- IPO or Lockup Expiration: Set a 10b5-1 plan before the window opens to avoid rushed decisions.

- Large Expenses Ahead: Use vested RSUs for goals such as a home purchase, charitable gift, or tuition.

- Rising Concentration: Reduce exposure when company stock becomes a large share of total wealth.

- Strong Market Conditions: Diversify gradually when valuations and liquidity are favorable.

Diversification works best when it happens by design, not by reaction.

RSU Strategies for Diversification

Most tech executives already understand the mechanics. The challenge isn’t knowledge; it’s time, bandwidth, and the discipline to follow through when markets get noisy. That’s where a well-built plan matters. The right structure adds accountability and helps you stay consistent even when headlines or stock moves tempt you to do the opposite.

Selling on a Schedule (10b5-1 Plans)

When your company’s stock is having a good run, the hardest part can be deciding when to sell. A 10b5-1 plan removes that guesswork. Once in place, it executes trades on a pre-set schedule, regardless of market noise.

Example: One exec set their plan to sell a fixed number of shares on the first trading day of each month for 18 months — no decisions to make, no temptation to “wait just a little longer.”

|

Benefit |

How It Helps |

Your Role / Our Role |

|

Removes emotion from selling |

Avoids panic selling in dips or holding too long in rallies |

You approve structure; we design plan with brokerage |

|

Smooths tax impact |

Spreads gains over multiple tax years |

We coordinate with your CPA |

|

Creates predictability |

Know your future cash flow from sales |

We monitor and adjust if needed |

Donor-Advised Funds (DAFs) & Charitable Giving

If giving is part of your plan, donating appreciated RSUs directly can offset taxes in the year of the gift. You avoid capital gains on the donated shares and get a deduction for the fair market value.

Example: An exec donated $250k of vested shares to a DAF, taking the deduction that year while granting the funds to charities over the next three years.

|

Benefit |

How It Helps |

Your Role / Our Role |

|

Tax efficiency |

Deduction now, no capital gains on donated shares |

You set giving priorities |

|

Flexibility |

Decide later which charities receive the funds |

We open and fund the DAF for you |

|

Aligns with values |

Turn concentrated wealth into impact |

We can coordinate with an organization on behalf of a client once an introduction is made |

Reallocating to a Diversified Portfolio

Selling RSUs is only half the equation — where you put the proceeds matters just as much. Reallocating into a portfolio that reflects your risk tolerance and life goals protects you from overexposure and creates new growth opportunities.

Example: An exec shifted 40% of their RSU sales into global equities, 30% into municipal bonds, 20% into private real estate, and 10% into an ESG-aligned fund that reflected their personal values.

|

Benefit |

How It Helps |

Your Role / Our Role |

|

Reduces concentration risk |

Limits exposure to a single company or sector |

You define comfort level; we recommend allocation |

|

Supports long-term goals |

Aligns with retirement, liquidity, or legacy planning |

We integrate into your broader financial plan |

|

Potential for smoother returns |

Diversified mix reduces volatility |

We rebalance as needed |

Advanced Strategies for Managing Concentrated Stock and Tax Exposure

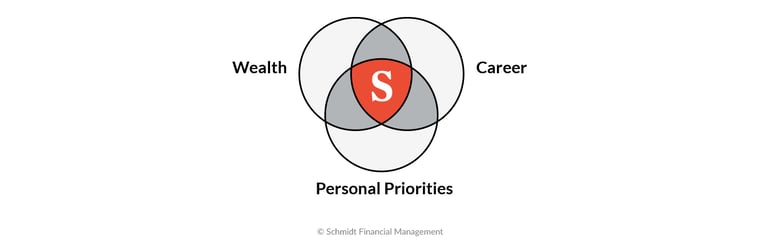

As wealth grows, complexity often grows with it. Equity that once felt like an opportunity can start to feel like a responsibility, a powerful asset that requires thoughtful management to keep working in alignment with broader goals.

For clients with significant company stock positions, certain advanced approaches can help create flexibility and balance. Exchange funds may offer diversification without triggering an immediate tax bill. Others choose to align charitable intentions with income planning through structures such as charitable remainder trusts. Ongoing tax-loss harvesting, whether automated or customized, can help manage gains as equity continues to vest.

The real focus is not on any single tactic but on building a framework that can evolve as life does. Schmidt FM works with clients to help navigate those turning points, bringing structure and perspective to moments when wealth, career, and personal priorities intersect.

When managed thoughtfully, equity can shift from a source of pressure to a source of balance. That is the kind of financial clarity we aim to foster.

The Advisor Advantage: Tax-Aware RSU Diversification

Diversifying RSUs is one thing. Doing it in a way that minimizes avoidable taxes is another. The difference often comes down to timing, coordination, and making sure every move fits your broader tax picture. That’s where guidance makes a tangible difference. Here’s a quick breakdown of how this works in practice, and how we help clients navigate it.

Advisor Advantage #1: Understanding Ordinary Income and Capital Gains

When RSUs vest, their fair market value is treated as ordinary income and added to your W-2. Selling right away means there’s no capital gain. Holding those shares introduces potential appreciation, which is taxed later as a capital gain.

|

Action |

Tax Treatment |

Impact |

|

Sell at vest |

100% taxed as ordinary income |

No capital gain exposure |

|

Hold more than one year post-vest |

Ordinary income at vest plus long-term capital gains on appreciation |

Lower tax rate on gains, higher market risk |

|

Sell within one year post-vest |

Ordinary income at vest plus short-term capital gains |

Gains taxed at higher ordinary income rate |

An advisor helps you model these outcomes in real terms, connecting each decision to liquidity needs, risk tolerance, and long-term goals.

Advisor Advantage #2: Multi-Year Tax Planning Support

Selling too much in a single year can create unnecessary tax friction. Spreading RSU sales across multiple years can smooth income and maintain flexibility for future vesting events.

|

Strategy |

Benefit |

Considerations |

|

Spread sales over several years |

Avoids bracket spikes |

Requires forward planning and coordination |

|

Front-load in lower-income years |

Takes advantage of temporarily lower tax rate |

Monitor for alternative minimum tax exposure |

|

Coordinate through a tax dashboard |

Visualize multi-year projections before selling |

Requires current income data for accuracy |

Advisors who work in step with CPAs can help map a multi-year plan that balances opportunity with tax efficiency.

Advisor Advantage #3: Coordinating Complex Tax Interactions

For executives with multiple types of equity — such as Incentive Stock Options (ISOs) or Qualified Small Business Stock (QSBS) — each decision can affect another. Selling too much stock in a single year could trigger the Alternative Minimum Tax (AMT) or impact eligibility for QSBS gain exclusions.

|

Tax Element |

Why It Matters |

How an Advisor Helps |

|

Alternative Minimum Tax (AMT) |

RSU sales increase taxable income, which can trigger AMT |

Sequence sales and exercises strategically in coordination with your CPA |

|

Qualified Small Business Stock (QSBS) |

Holding periods and eligibility rules determine whether gains can qualify for exclusion |

Verify eligibility and align timing with other transactions |

An advisor helps you see these interactions in context so that no single move works against the rest of your plan.

Integrating RSUs Into a Larger Financial Strategy

Funding Future Goals

Your RSU sales can accelerate timelines on major life goals without derailing your investment strategy.

Example:

- Using part of a sale to fully fund a 529 plan for each child, locking in years of tax-free growth.

- Allocating a portion to a “seed fund” for a future startup or investment property.

|

Goal |

RSU Strategy |

Impact |

|

Education |

Fund 529s in one lump sum |

Maximize compounding over time |

|

Entrepreneurship |

Set aside cash for future venture |

Avoid tapping retirement assets later |

|

Real estate |

Use proceeds for down payment |

Diversify into tangible asset class |

Protecting Wealth While Maintaining Upside

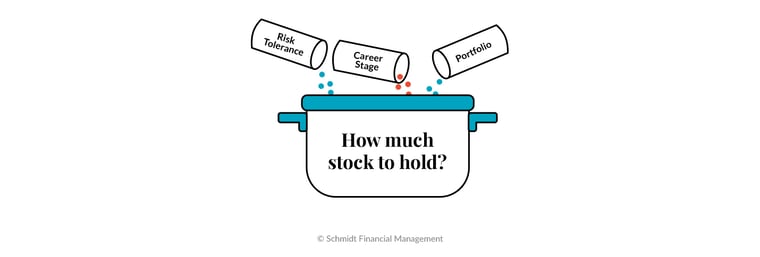

Diversification protects you from having your financial life move in lockstep with a single company’s stock. How that looks in practice will be different for everyone, depending on comfort with risk, career stage, and other assets already in play.

At Schmidt FM, there’s no preset percentage or formula for how much company stock to hold. The right mix depends on risk tolerance, career stage, and the rest of the portfolio. For some, that means gradually selling specific tax lots to manage exposure and control taxable gains. For others, it’s reallocating proceeds into diversified funds, bonds, or alternative assets that align with long-term goals. The focus is on progress that feels intentional and coordinated, not abrupt or reactive.

|

Focus Area |

Purpose |

Outcome |

|

Thoughtful reduction of concentrated positions |

Manage exposure without sudden shifts |

Lower correlation between income and portfolio performance |

|

Tax-aware sale of specific lots |

Control realized gains during diversification |

Keep long-term tax efficiency in view |

|

Reinvestment into diversified funds and fixed income |

Broaden sources of potential return and stability |

Create a foundation that supports growth through market cycles |

Protecting wealth while maintaining upside is about approaching your finances with the same clarity and purpose that have driven your career.

Reinvesting in Alignment with Personal Priorities

RSUs can also help you align your money with what matters most to you, whether that’s socially responsible investing, philanthropy, or creating dependable income streams.

Example: An executive split RSU proceeds into three buckets — a U.S. ESG-focused equity fund, a municipal bond fund for tax-free income, and a donor-advised fund for ongoing charitable giving.

|

Priority |

Allocation Idea |

Benefit |

|

Values-based investing |

U.S. ESG or sustainability-screened equity fund |

Align portfolio with personal and environmental values |

|

Income generation |

Municipal bond funds or high-quality dividend ETFs |

Aim to create steady, tax-efficient income stream |

|

Philanthropy |

Donor-advised fund |

Immediate deduction and flexible, ongoing charitable impact |

Ready to Build a Smarter RSU Strategy?

Your RSUs can be one of the most powerful drivers of long-term wealth if they’re integrated into your broader financial plan. The key is aligning your equity strategy, tax planning, and investment goals so each decision works together, not in isolation.

If this question causes you to lose too much sleep at night then it's time to work with an advisor like Schmidt. We aim to help clients diversify wisely, focusing on tax-efficiency, making a clear plan for what comes next.

Quick Glossary: RSU Diversification Terms

- Concentration Risk: The risk of having too much wealth tied to one company’s stock, leaving your income and portfolio exposed to the same market forces.

- 10b5-1 Plan: A preset trading plan that allows company insiders to sell stock automatically on a fixed schedule, removing emotion and helping avoid insider trading issues.

- Vesting: The moment your RSUs become yours. The value is taxed as ordinary income whether you sell or not.

- Capital Gains: The profit earned from selling an investment for more than its purchase price. Long-term gains (held over one year) are taxed at lower rates.

- Exchange Fund: A pooled investment that allows investors to swap concentrated stock positions for a diversified portfolio without triggering an immediate tax bill.

- Qualified Small Business Stock (QSBS): Stock that may qualify for up to 100 percent exclusion of capital gains if specific IRS conditions are met and holding periods are satisfied.

- Donor-Advised Fund (DAF): A charitable account that lets you donate appreciated stock, take a tax deduction immediately, and decide later which nonprofits receive the funds.

- Tax-Loss Harvesting (TLH): Selling investments at a loss to offset taxable gains.

- Charitable Remainder Trust (CRT): A trust that provides income to you or another beneficiary for a period of time, with the remaining assets going to charity—often used to reduce taxes on large stock sales.

- Alternative Minimum Tax (AMT): A secondary tax calculation that can impact high earners with large stock-based income or deductions. Coordinating timing with your CPA helps manage exposure.

RSU Diversification FAQs

What’s a healthy percentage of my net worth to keep in company stock?

There isn’t a universal percentage that works for everyone. The right balance depends on your overall financial picture, risk tolerance, career stage, other assets, and how dependent your income already is on your company’s success. At Schmidt FM, we help clients find that point of balance by modeling different scenarios and adjusting over time as equity, cash flow, and goals evolve.

If I sell, won’t I miss future upside?

Maybe, but diversification doesn’t mean you’re out of the game. It means you’re managing what you’ve already earned. It's not uncommon for tech professionals to keep a defined portion of stock for potential upside while moving the rest into a balanced mix of funds and bond strategies that can grow steadily regardless of what happens with one ticker.

How do I diversify without creating a big tax bill?

Timing and coordination. We often spread sales over multiple years to smooth income and use tax-loss harvesting to offset realized gains. Schmidt advisors take into account the unique account needs for clients and base management on criteria that serves the clients best interest.

What do you invest RSU proceeds in once they’re sold?

We aim to diversify portfolios using investment vehicles that match the clients unique needs. The goal is stability, consistency, and alignment with your overall financial plan. Each portfolio is customized around your timeline, risk tolerance, and liquidity needs.

What’s the biggest risk of not diversifying?

Correlation. When your income, bonus, and equity all rely on one company, a single downturn can hit you three times over. Diversification spreads that risk so your personal financial life isn’t moving in lockstep with your employer’s stock.

When is the right time to start diversifying?

Usually before you feel like you have to. The best time is when you can plan calmly, not react quickly. Common inflection points include IPO lockup expirations, large vesting events, or when company stock starts to represent more than half of your total net worth.