July 29, 2026

Don't leave equity—or cash—on the table.

As a senior-level tech professional, your compensation is more than a salary—it's a complex ecosystem of equity, tax-advantaged tools, and insurance benefits that can significantly impact your long-term wealth. The challenge isn’t understanding that these benefits exist. It’s having the time and strategic guidance to make the most of them.

At Schmidt Financial Management, we work with tech executives who often receive equity grants that may represent a substantial portion of their compensation and have already built $5M+ in investable assets. These clients are ambitious, discerning, and busy. They’re not looking for generic advice—they want a partner who understands how to align their benefits with broader financial goals, from minimizing taxes to accelerating financial independence.

[Read on below]

[Continued]

In this guide, we’ll walk through the key components of a typical benefits package—from equity compensation to retirement plans—offering insight into how each element can function as a lever in your overall wealth strategy. Whether you're managing a new grant, evaluating your 401(k) options, or planning around your HSA, this is about taking a structured, high-level view of your benefits—and using them to work smarter, not harder.

What Are Employee Benefits?

Employee benefits are non-salary compensation your employer provides—often representing a significant portion of your total rewards package. For tech leaders like Directors, VPs, and senior engineers at companies such as Amazon, Microsoft, or late-stage startups, benefits often go far beyond health coverage and retirement plans. They include equity grants, tax-advantaged accounts, and wealth-building tools that, if managed strategically, can support long-term goals like financial independence, liquidity, and multigenerational planning.

At your level, optimizing these benefits isn’t just about saving money—it’s about structuring them to work as part of your larger financial strategy. Here's how the most common benefit types typically show up in practice:

- Restricted Stock Units (RSUs): Company shares granted to you as part of your compensation, which vest over time (e.g., quarterly over four years). RSUs are taxed as income when they vest, and may grow significantly depending on your company’s performance. A sound tax strategy and diversification plan are essential to avoid overconcentration risk.

- 401(k) with Employer Match: A tax-deferred retirement account you can fund with pre-tax dollars (up to the IRS limit). Many companies match a portion of your contributions—e.g., Amazon contributes 50% of the first 4% you put in—effectively giving you free money toward retirement.

- Employee Stock Purchase Plan (ESPP): Lets you buy company shares at a discount (typically 10–15%) using after-tax payroll deductions. Some plans include a lookback provision that allows you to buy stock at the lowest price during a purchase window. When managed wisely, ESPPs can be a relatively low-risk way to build wealth.

- Health Insurance: Comprehensive medical, dental, and vision coverage for you and your dependents, often effective on your first day. Plan types vary—high-deductible plans, PPOs, or HMOs—and the right choice depends on your health needs, preferences for provider flexibility, and whether you want to leverage a Health Savings Account (HSA).

These benefits aren’t static. Vesting schedules shift, plan offerings evolve, and your financial picture changes. Understanding how each component interacts with your compensation and wealth planning goals is where real value is unlocked.

Why It’s Worth Working With a Financial Advisor on Your Benefits Package Strategy

You already know your benefits package carries significant financial weight—especially when equity, taxes, and timing are involved. What most senior tech professionals don’t have is the bandwidth to analyze every moving piece or stay ahead of changing rules and opportunities.

That’s where we come in. At Schmidt Financial Management, we work with high-level tech professionals—people managing multi-layered compensation, navigating liquidity events, or planning for early retirement. We understand the stakes and know how to turn a dense benefits package into a streamlined, tax-efficient wealth strategy.

This guide highlights what to look for—and where a strategic advisor can take the work off your plate while keeping your financial plan moving forward.

Employee Benefit Package Options

Most tech professionals know the basics of what their benefits include—but not always how those pieces fit into their broader financial life. That’s where we come in.

From health insurance and tax-advantaged accounts to equity compensation and retirement planning, your comprehensive benefits package is full of opportunities to build wealth, reduce risk, and protect your future.

The challenge? These tools come with rules, trade-offs, and time-sensitive decisions. And not all options are created equal.

Below, we’ll walk through the most common types of employee benefits, explain what they really mean, and highlight where thoughtful planning can make a meaningful difference. If you’ve ever wondered what to do with RSUs, how much to contribute to your 401(k), or whether to use an HSA, you’re in the right place.

- Health-Related Benefits

- Retirement Planning Benefits

- Equity Compensation Benefits

- Insurance and Protection Benefits

1. Health-Related Benefits

Health benefits are often where thousands of untapped dollars sit—either in the form of missed tax advantages, poorly chosen plans, or underutilized accounts. Many of these benefits come with contribution limits, reimbursement rules, and deadlines that require a level of attention most employees don’t give them. Understanding the mechanics of HSAs and FSAs helps you optimize for tax efficiency, liquidity, and long-term planning.

Health Insurance

Many employers provide health insurance, which typically covers medical, dental, and vision. Some plans may also cover alternative care like counseling, chiropractic treatments, acupuncture, or even massage therapy. These types of care are often underused, but they can help support work-life balance, burnout prevention, and overall performance for ambitious executives or senior leaders, so they are worth investigating.

Health insurance plan types you might see:

- Health Maintenance Organization (HMO): Lower premiums and costs, but limited to a network of providers.

- Preferred Provider Organization (PPO): Higher flexibility to choose doctors, with slightly higher costs.

- High-deductible health plans (HDHPs): Lower monthly premiums but higher out-of-pocket costs—often paired with HSAs.

- Point of Service (POS) Plans: Combine features of HMOs and PPOs, but require referrals for specialists.

There’s no one-size-fits-all answer here. A healthy single person might benefit from an HDHP and an HSA, while someone with ongoing medical needs might be better off with a PPO despite the higher premiums. The key is to evaluate total cost—not just what comes out of your paycheck.

Health Savings Account Planning (HSA)

If your health insurance is a high-deductible plan (HDHP), you likely qualify for an HSA—and it can be a powerful tool in your financial toolkit.

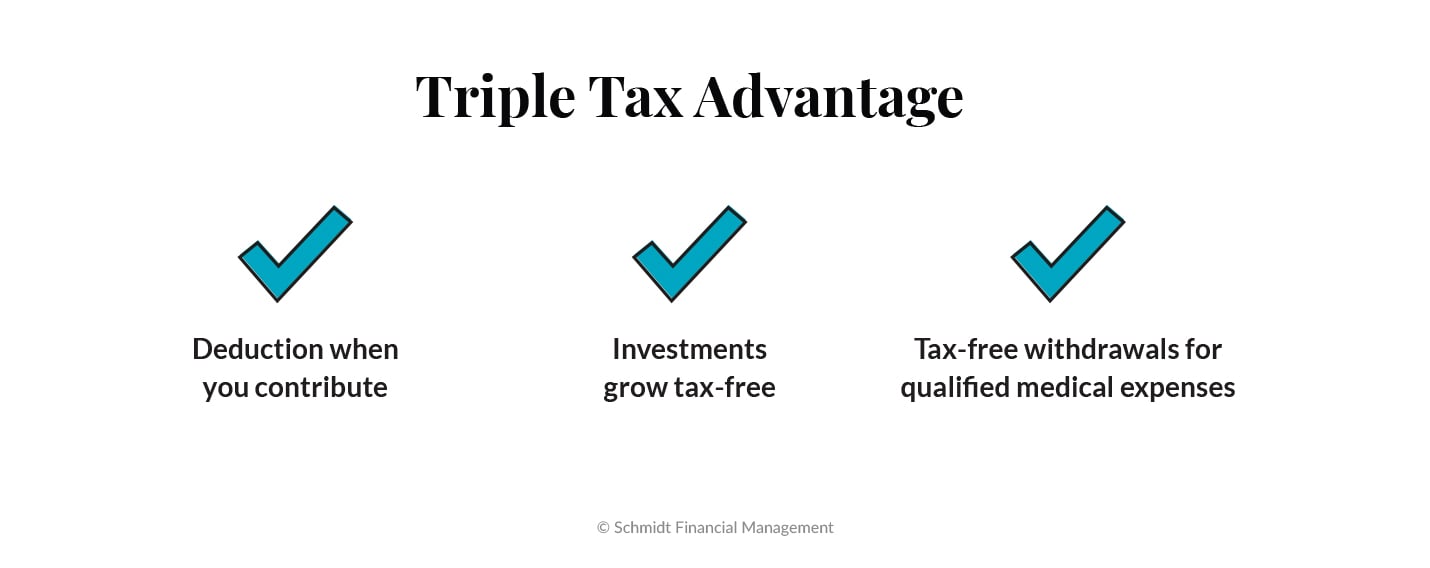

- Triple tax advantage: You get a tax deduction when you contribute, your investments grow tax-free, and withdrawals for qualified medical expenses are also tax-free. No other account works this way.

- Long-term growth: Funds roll over year to year and can be invested, which means you can use your HSA as a stealth retirement account for healthcare costs later in life.

- Flexible use: You can use HSA dollars for everything from prescriptions and copays to dental work and eyeglasses.

- Contribution limits for 2026: Up to $4,400 for individuals and $8,750 for families (plus an extra $1,000 catch-up contribution if you’re 55+).

We often recommend clients max out their HSA if they can afford it—it’s a smart move for both health costs and long-term planning.

Flexible Spending Account Planning (FSA)

Unlike HSAs, FSAs don’t require a specific type of insurance—but they do require careful timing.

- Tax savings: You contribute pre-tax dollars to cover eligible medical, dental, vision, or dependent care expenses.

- Use it or lose it: Most FSAs have a year-end deadline. Some employers offer a short grace period or allow you to roll over a small amount, but for the most part, unspent funds are forfeited.

- Contribution limits for 2026: Up to $3,400 for health FSAs; up to $7,500 for dependent care FSAs (per household).

- Good for predictable expenses: FSAs work best when you know you’ll have out-of-pocket costs—like ongoing prescriptions, child care, or planned dental work.

We help clients plan FSA contributions around life events (like the birth of a child) or big-ticket expenses, so they avoid leaving money on the table.

At Schmidt Financial Management, we help clients look beyond the obvious, ensuring that benefits like HSAs and FSAs support their cash flow and tax strategy and that their health insurance actually aligns with their risk profile and usage patterns.

2. Retirement Planning Benefits

Retirement benefits are one of the most powerful tools employers offer—and yet, many people contribute without a strategy. These plans can do much more than just help you “save for the future.” With proper planning, they may reduce your tax bill today, create long-term compounding growth, and help you build financial independence earlier than you might expect.

401(k) Plans

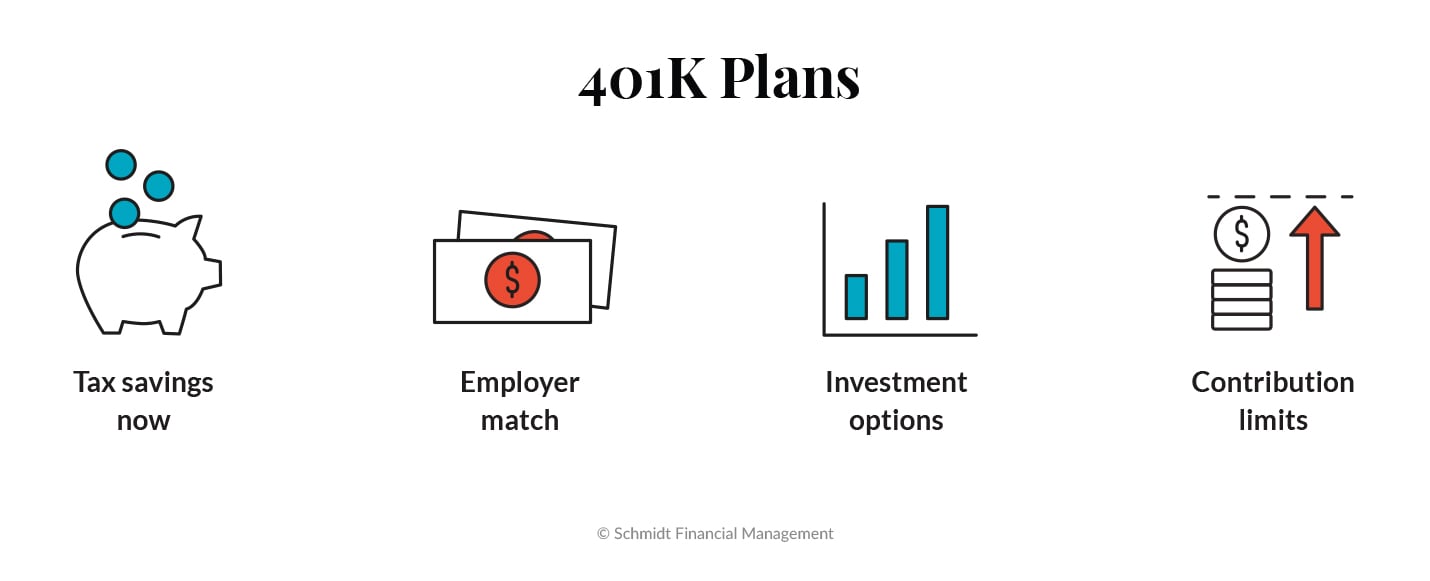

The 401(k) remains one of the most common—and valuable—retirement savings vehicles offered by tech companies.

- Tax savings now: Contributions are made pre-tax (traditional), lowering your taxable income in the year you contribute, or after-tax (Roth), which allows you to make tax-free withdrawals (qualified distributions). Both offer a type of discount for savings.

- Employer match: Many companies match a portion of your contributions. If you're not contributing enough to get the full match, you're literally missing part of your compensation.

- Investment options: Most plans offer a curated list of mutual, target-date, and index funds. Some companies also offer a brokerage window for more flexibility.

- Contribution limits: In 2026, you can contribute up to $24,500 if you're under 50, or $32,500 with catch-up contributions if you’re 50 or older.

A smart 401(k) strategy isn’t just about contributing—it’s about how much to contribute, which investments to select, and how your 401(k) fits into your broader portfolio and tax picture. We help clients understand what type of 401(k) makes the most sense, how to manage risk across accounts, and how to plan for eventual withdrawals.

Deferred Compensation Plans/Programs (DCP)

Some companies—particularly in the public, academic, or large corporate sectors—offer nonqualified deferred compensation plans to senior-level employees. These are not widely available, but when offered, they can play a significant role in high-income tax and retirement strategies.

DCPs allow you to defer a portion of your compensation beyond traditional 401(k) limits. Contributions are typically made pre-tax, which can reduce your current tax liability and shift income to a future year—often when your tax rate may be lower. Used strategically, they create additional space for tax-deferred growth and potential income streams in retirement.

These plans are highly customizable and complex, with liquidity, tax timing, and employer risk implications. Working with an advisor experienced in DCPs is essential to avoid costly missteps and ensure the benefit is integrated into your broader wealth strategy.

3. Equity Compensation Benefits

Equity compensation is a highly utilized benefit that provides you with ownership in the company you work for. This compensation may include employee stock options, restricted stock units (RSUs), and employee stock purchase plans (ESPPs). Understanding how they work—along with the tax implications and vesting schedules—is crucial to managing them effectively.

Employee Stock Purchase Plan (ESPP)

An ESPP lets you buy your company’s stock at a discount—typically up to 15%—using after-tax payroll deductions. While it may seem simple, the right strategy can significantly enhance the value of this benefit.

- Discounted purchase: Shares are often bought at a discount based on either the price at the beginning or end of the offering period (whichever is lower), giving you an immediate gain.

- Automatic investing: Contributions are deducted from each paycheck, making it an easy and consistent way to invest.

- Tax complexity: The timing of your sale affects how much tax you owe. Holding periods and qualifying dispositions matter—a lot.

- Integrated strategy: Whether to hold or sell your ESPP shares depends on your overall portfolio, company stock concentration, and tax situation.

We help clients design ESPP strategies that align with their cash flow, risk tolerance, and tax planning goals—turning a simple payroll deduction into a valuable wealth-building tool.

Restricted Stock Units (RSUs)

Restricted stock units are a form of equity compensation that grants company shares over time, typically based on a vesting schedule. They may seem straightforward on the surface but they carry important tax and planning implications.

- Vesting triggers income: RSUs are taxed as ordinary income when they vest—not when you sell—so they can create a surprise tax bill if you’re unprepared.

- Stock price matters—but is not everything: While upside potential is real, RSUs still have value even if the stock is flat or down—because you're receiving shares at no cost.

- Liquidity + concentration: Once vested, RSUs increase your exposure to your employer’s stock. Deciding whether to hold or sell should be based on your broader financial plan, not just sentiment.

- Not the same as restricted stock: RSUs don’t require a purchase or 83(b) election—key differences that impact tax treatment and flexibility.

If RSUs are a big part of your compensation, proactive tax planning and diversification strategies can help you avoid concentrated risk and optimize your take-home value.

4. Insurance and Protection Benefits

Insurance benefits may not drive your compensation negotiations, but they play a critical role in protecting your income, dependents, and long-term financial stability.

These protections help safeguard your income, your dependents, and your overall financial plan—especially in the event of illness, injury, or death. Many tech professionals overlook or underutilize these options, missing out on low-cost ways to reduce risk and preserve wealth.

Life and Disability Insurance

Most employers offer some level of group life and disability coverage as part of the standard benefits package. But default coverage isn’t always enough—especially if you have dependents or significant financial obligations. We highly recommend working with your financial advisor to ensure your insurance is suitable for your current income level and future needs if something were to happen to you.

- Life Insurance: Group life policies often provide coverage equal to 1–2x your salary. While this is a helpful baseline, it may fall short of your family’s actual needs. Supplemental life insurance through your employer can be cost-effective and easy to obtain—often without a medical exam.

- Short-Term Disability (STD): Covers a portion of your income if you’re temporarily unable to work due to injury, surgery, or medical leave (including maternity leave in many cases). It usually kicks in after a brief waiting period.

- Long-Term Disability (LTD): If an injury or illness keeps you out of work for months or even years, LTD replaces a portion of your income—typically 50–60%. This is one of the most critical (and underrated) benefits for high earners.

- Tax considerations: Whether your disability benefits are taxable depends on who pays the premiums—something we evaluate carefully when building out cash flow and insurance strategies.

How To Maximize Your Employee Benefits

At Schmidt Financial Management, we believe that the key to unlocking the full potential of your employee benefits lies in three core strategies: understanding your options, planning strategically, and reviewing regularly. Let’s break it down.

1. Understand Your Options

Your benefits package can seem overwhelming when you start a new job or go through open enrollment. But to make the most of it, you need to start by understanding what's available to you. Take the time to carefully review your benefits during onboarding or your annual benefits review period. Attend any benefits information sessions your employer offers—these are designed to help you navigate your options and answer questions about the finer details of the plans. And when things feel unclear, don’t hesitate to ask questions.

At Schmidt FM, we’re here to help you make sense of these offerings. We can walk you through the intricacies of your employee benefits, ensuring you don’t miss out on any valuable opportunities. We specialize in helping tech professionals, like you, optimize their compensation packages.

2. Plan Strategically

Once you understand your options, the next step is aligning your benefits with your personal financial goals. Each benefit—whether it's your 401(k) contributions, HSA contributions, or RSUs—offers unique tax advantages and growth opportunities.

For instance, how much should you contribute to your 401(k) to get the full company match without over-committing in the short term? Are you maximizing your HSA for its triple tax advantages? Are you taking full advantage of your stock options without triggering unnecessary taxes? These are the types of questions that can significantly impact your financial future.

At Schmidt FM, we don’t just offer tax planning; we provide personalized strategies to help you optimize each benefit for maximum impact. Whether it’s advising you on how to balance retirement savings with current cash flow or guiding you through the complexities of equity compensation, our goal is to ensure your benefits work in concert with your long-term financial goals.

3. Regular Review

The final step in maximizing your employee benefits is regular review. Employee benefits aren’t static—they change as you progress in your career, shift roles, or go through significant life events. That means your benefits package should evolve along with you. Life changes like marriage, homeownership, or the birth of a child can impact your healthcare needs and financial priorities. Not to mention, your company’s offerings may change over time, with new benefits introduced or old ones modified.

That’s why it’s crucial to reassess your benefits annually during open enrollment or whenever significant life events occur.

Schmidt FM offers ongoing benefits and financial planning reviews to help you stay on track. We work with you to ensure your benefits remain aligned with your life’s shifting needs, so you’re always positioned for success. Our team provides proactive planning to hopefully maximize every aspect of your compensation package, ensuring that you're as prepared as you can be for whatever the future holds.

Maximize Your Employee Benefits Package With Schmidt Financial Management

Your employee benefits package is more than just pesky HR paperwork—it’s a toolkit for building financial security, protecting your health, and planning for the future. Yet many professionals leave money on the table by not fully understanding what’s available. At Schmidt Financial Management, we help you unlock the full value of your benefits, so every contribution you make or grant you receive positions you to receive the highest impact.

💡 Want to make the most of your benefits? Check out what a Schmidt client looks like and decide if it's time to book an introductory meeting.

Frequently Asked Questions About Employee Benefits Packages

1. How can I avoid overconcentration risk with my RSUs?

Diversification is key. We help you develop a tax-efficient selling plan that balances holding shares for growth with mitigating risk from having too much of your net worth tied to one company’s stock.

2. What is equity compensation?

Equity compensation is a form of non-cash pay that companies offer to employees, often in the form of stock options, restricted stock units (RSUs), or employee stock purchase plans (ESPPs). It allows employees to share in the company’s growth and success by owning part of the business. Equity compensation can help build long-term wealth but also comes with important tax, timing, and diversification considerations.

3. What’s the optimal way to leverage my 401(k) match without overcommitting cash flow?

Contribute at least enough to capture the full employer match—it’s free compensation. Beyond that, we analyze your overall cash flow and tax situation to recommend the ideal contribution level that maximizes savings without creating liquidity strain.

4. How should I approach my Employee Stock Purchase Plan (ESPP) to maximize returns and minimize taxes?

Timing your purchases and sales to meet qualifying disposition rules is crucial. We craft a personalized strategy to optimize your ESPP discounts while managing tax impacts, aligning this with your broader portfolio and risk tolerance.

5. What advantages do Health Savings Accounts (HSAs) offer for high earners?

HSAs provide triple tax benefits—contributions are tax-deductible, investments grow tax-free, and qualified withdrawals are tax-free. For busy executives, HSAs can double as a stealth retirement account for future healthcare expenses.

6. How do Deferred Compensation Plans (DCPs) fit into my tax and retirement strategy?

DCPs allow you to defer income beyond 401(k) limits, potentially lowering your current tax bill and shifting income to future years. We evaluate employer terms and tax timing to integrate DCPs effectively into your long-term wealth plan.

7. What’s the best way to handle ISOs vs. NSOs—and how do I avoid AMT surprises?

Incentive Stock Options (ISOs) and Non-Qualified Stock Options (NSOs) come with very different tax implications. ISOs may qualify for favorable long-term capital gains treatment, but they can also trigger Alternative Minimum Tax (AMT) if exercised without a clear strategy. NSOs are taxed as ordinary income at exercise, which simplifies some decisions but limits flexibility. We help clients model different exercise timelines to minimize tax exposure, manage AMT risk, and align option strategies with broader liquidity and diversification goals.

8. Can I use a Mega Backdoor Roth strategy to expand my tax-free retirement savings?

Yes—if your 401(k) plan allows after-tax contributions and in-plan Roth conversions or in-service rollovers, the Mega Backdoor Roth can be a powerful tool to significantly expand your Roth savings. This strategy allows you to contribute well beyond traditional Roth limits, potentially adding $30K+ per year in tax-advantaged growth. We evaluate plan provisions, contribution sequencing, and your overall cash flow to implement this effectively and avoid common pitfalls.

9. How do I ensure my insurance coverage is adequate for my income and family needs?

Group life and disability insurance provided by employers are often insufficient for high earners. We assess gaps and recommend supplemental policies to protect your income and dependents without unnecessary expense.

10. What benefits can I expect from working with Schmidt Financial Management on my employee benefits?

We save you time and reduce complexity by proactively helping you manage your benefits package. This includes guidance aimed at helping you optimize tax strategies, aligning benefits with your financial goals, and providing ongoing reviews to adapt as your situation evolves.

11. How often should I review and adjust my benefits strategy?

At minimum, annually during open enrollment. But also whenever you experience major life changes (e.g., marriage, new child) or job transitions. Regular reviews ensure your benefits remain aligned with your evolving financial plan.

12. How do I balance maximizing tax-advantaged accounts with maintaining liquidity?

It’s a strategic balance. We help you determine the right allocation between tax-deferred accounts, taxable investments, and liquid reserves to maintain flexibility while optimizing long-term growth and tax efficiency.

*This blog was updated March 14, 2026, to reflect 2026 contribution limits.