February 24, 2026

Next in our series on Restricted Stock Units (RSUs) is the topic of selling or holding RSUs when they vest. Let’s dive into this common dilemma and explore some strategies to help you make the best choice for your financial future.

How Restricted Stock Units (RSUs) Work

Before we delve into the sell-or-hold debate, let’s quickly recap what RSUs are:

- RSUs are a form of equity compensation granted by your employer.

- They vest over time according to a predetermined schedule.

- Once vested, RSUs are treated as income and subject to income tax.

RSUs are company stock subject to vesting conditions, meaning they have no actual value until the vesting requirements are met. (Remember that RSUs aren’t the same as stock options or ESPPs—there’s no purchase required, and no strike price to worry about. )

Now, let’s explore the pros and cons of selling versus holding your RSUs.

Factors to Consider When Deciding to Sell RSUs

Take someone who’s been at Microsoft for 12 years.

They’ve received new RSU grants every year — so at this point, they’re juggling three or four different vesting schedules, each with its own tax timing and expiration dates.

Before that, they spent eight years at Meta, and still hold several tranches of those vested shares.

Add in a couple of major salary jumps, a few big bonuses, and they’re now squarely in the 35%+ federal bracket, which means that flat 22% RSU withholding hasn’t covered their true tax rate in years.

Last year, a large vest pushed their income high enough to trigger the Alternative Minimum Tax (AMT) for the first time, a secondary tax calculation that kicks in when income spikes or certain deductions phase out.

This year, they’re trying to decide whether to sell, hold, or exercise other equity awards — all while keeping their long-term goals on track and their tax bill predictable.

That’s the point where managing equity stops being a side task and starts requiring an integrated strategy that accounts for vesting timelines, tax exposure, and concentration risk across multiple employers.

At Schmidt Financial Management, that’s exactly what we do.

We build a comprehensive model that helps map vesting schedules, anticipates possible tax implications, while working to coordinate your equity decisions with your overall financial plan - so you can stay focused on your career, knowing you are not alone in managing the moving pieces.

Tax Implications: Selling vs. Holding Your RSUs

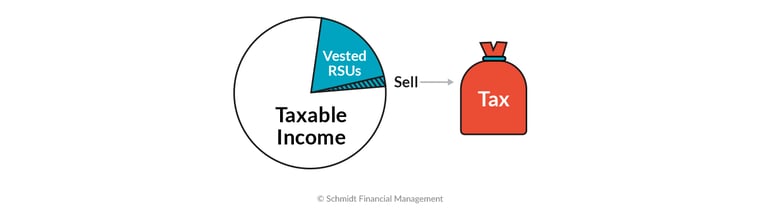

There’s a reason you need to report your RSUs on your taxes and that’s because selling Restricted Stock Units (RSUs) can have significant tax implications.

When your RSUs vest, they instantly create taxable income, even if you don’t sell a single share. That’s the key distinction to understand before deciding whether to sell or hold.

At vest:

- The fair market value of the shares that vest is taxed as ordinary income, just like your salary or bonus.

- Most companies automatically withhold taxes at the IRS supplemental wage rate: 22% federally (or 37% for income over $1 million).

- Those withheld shares are effectively sold on your behalf, leaving you with the rest.

The problem is that this flat withholding rate often underestimates what you actually owe if your total income puts you in a higher bracket (32%, 35%, or 37%).

Whether you sell or hold, the IRS treats the vest as income; only selling can give you liquidity to cover the true tax bill.

If you sell immediately

Selling at vest (often called a “sell-to-cover” or “same-day sale”) can feel transactional, for some it can be a choice toward simplifying your life:

- You lock in the vesting value, so there’s no capital gains exposure.

- You have cash on hand to cover taxes, diversify, or fund other goals.

- It can prevent a mismatch between your tax bill and liquidity, avoiding an April surprise.

The trade-off: you miss potential upside if your company’s stock price climbs, and you’ll need to decide where to reinvest those proceeds.

If you hold after vesting

Holding converts that income-taxed stock into an investment decision and introduces new tax dynamics:

- Any future gain (or loss) is taxed as capital gains when you eventually sell.

- Short-term (<1 year): taxed at your ordinary income rate.

- Long-term (>1 year): taxed at 15–20% federally, depending on income.

- If the stock price falls, your vested value (and potential tax benefit) can erode quickly.

- Selling at a loss within 30 days of repurchasing similar shares can trigger a wash sale, disallowing that loss.

In other words, holding may unlock better tax rates, but it also exposes you to market and concentration risk, plus additional tax complexity if you trade around your position.

Should I Sell My RSUs When They Vest? Here Are Your Options

Even for those holding some shares, planning ahead matters. Sell too soon and it can feel like the IRS wins. Hold too long and a market dip can erase what was gained. The key is building a strategy that fits both risk tolerance and long-term goals. Here are a few ways to do that.

The RSU Hybrid Approach

While many professionals lean towards either selling or holding entirely, there’s a middle ground that’s worth considering: the hybrid approach. When considering the hybrid approach, it's important to evaluate the company's stock performance and future prospects. This strategy involves selling a portion of your RSUs while holding onto the rest.

Here’s how it works:

- Sell enough shares to cover taxes: This ensures you’re not caught off guard by a hefty tax bill.

- Diversify a portion: Sell some additional shares to invest in other assets, reducing your overall risk.

- Hold the remainder: Keep a portion of your RSUs to potentially benefit from future company growth. The shares you hold onto, if held for at least a year, also can give you the added benefit of the long-term capital gains rate.

This balanced approach allows you to enjoy the benefits of both selling and holding, while mitigating some of the risks associated with each strategy.

|

Pros |

Cons |

|

Provides immediate liquidity and covers taxes upfront |

Still exposes you to some company-specific volatility |

|

Reduces concentration risk through diversification |

Requires periodic monitoring and rebalancing |

|

Keeps some exposure to future company growth |

Adds a layer of complexity at tax time |

|

May qualify for long-term capital gains rates on held shares |

Can be emotionally tricky if stock prices fluctuate after selling |

The Long-Term Hold Strategy

If you believe in your company’s long-term growth and can tolerate some volatility, a long-term hold strategy may make sense. By keeping your RSUs for more than one year after they vest, you can qualify for lower long-term capital gains tax rates when you eventually sell.

|

Pros |

Cons |

|

Eligible for lower long-term capital gains tax (typically 15–20%) |

Increased exposure to company-specific risk |

|

Potential to capture future stock appreciation |

Stock volatility can erode paper gains before you sell |

|

Allows time to ride out short-term market swings |

Ties up capital that could be diversified elsewhere |

|

Simple to execute — just hold your vested shares |

Must plan for the tax bill at vest, even if you don’t sell |

The "Reinvest in Tax-Advantaged Accounts" Strategy

Even though RSUs can’t be fully sheltered in tax-advantaged accounts, they can still play a key role in a broader tax-efficient plan. Selling shares and using the proceeds to max out 401(k), IRA, or 529 contributions helps manage taxes today while building wealth for the future. It’s a simple way to turn a liquidity event into long-term progress.

|

Pros |

Cons |

|

Reduces current-year taxable income through pre-tax contributions |

Contribution limits may cap how much you can move each year |

|

Builds long-term, tax-deferred (or tax-free) retirement savings |

You’ll still owe taxes on RSUs at vest before reinvesting proceeds |

|

Improves diversification across asset classes |

Requires careful timing around vesting and payroll cycles |

|

Aligns RSU income with long-term financial goals |

Funds in retirement accounts are generally less accessible before age 59½ |

This strategy works best for high earners in technology who already have liquidity from other sources and want to turn equity income into lasting, tax-efficient wealth.

The Power of Periodic Review

Managing RSUs alone means juggling vesting schedules, tracking the stock, and remembering to rebalance in the middle of a busy life. Schmidt Financial Management steps in as a partner that brings structure, insight, and a rhythm you can rely on.

We monitor holdings, pay attention to market conditions, and flag the moments when action matters, whether that’s selling shares, adjusting a tax strategy, or reallocating investments. It’s similar to the gap between having a gym membership and working with a trainer. One offers access. The other can create better results because there is guidance, accountability, and a clear plan forward.

This is the value of periodic review. It turns equity from something that feels static into something active, coordinated, and intentionally managed.

Advanced FAQs: Selling Your RSUs

1. When’s the best time to sell my RSUs?

For most executives, selling at vest or soon after is the most efficient move. It locks in value, covers your tax bill, and reduces concentration risk. The exception is if your exposure is modest and you have a clear reason to hold for long-term capital gains.

2. Should I always sell immediately when shares vest?

Not always, but you should always decide intentionally. Selling at vest eliminates market risk and liquidity issues. Holding can make sense if you have strong conviction in your company and room in your portfolio to absorb volatility.

3. How much should I sell when my RSUs vest?

It often makes sense to sell enough to cover the tax bill while using the rest to diversify. Many of our clients use a hybrid approach: selling some to reduce overall risk while keeping some shares for the potential upside they may offer in the future. The right mix depends on your tax bracket, exposure, and goals.

4. What if my company only withholds 22% but I’m in a higher tax bracket?

Plan ahead. High-income earners often owe 32–37%, so the 22% default won’t cover your total liability. We help clients sell extra shares or make estimated payments after each vest to stay ahead of taxes.

5. What happens if I hold after vesting and the stock drops?

You’ll still owe tax on the value at vest, even if the price falls later. That’s why some executives choose to sell early to avoid paying taxes on income that disappears with market swings.

6. Can I sell during blackout periods?

Yes, if you have a 10b5-1 trading plan in place. It lets you pre-schedule trades that execute automatically during open windows, ensuring compliance while keeping your diversification plan on track.

7. What’s the best way to diversify after selling?

For some tech professionals, redirecting RSU proceeds into a mix of broad-market ETFs, bonds, or tax-advantaged accounts like a 401(k) or IRA can be an adequate solution. But a benefit of working with Schmidt is receiving more catered guidance that takes your unique goals and positions into account. We can work with you to structure reinvestment plans that align with your liquidity needs and tax outlook. This is when working with an experienced advisor can create tax alpha that can potentially be a game changer.

8. Should I hold some shares for long-term capital gains?

Only if the position is small relative to your overall net worth. The long-term capital gains rate (15–20%) can help, but not if your risk exposure outweighs the tax benefit.

9. What percentage of my wealth should be in company stock?

A healthy plan limits how much of a balance sheet depends on one company’s stock. When too much wealth sits in a single position, financial stability starts to rise and fall with that company’s performance. Reducing that exposure over time creates more flexibility, better risk management, and a clearer path forward.

10. How can Schmidt Financial Management help?

We help clients build a clear, actionable plan for selling RSUs, aligned with their vesting schedule, tax exposure, and broader financial goals. Timing decisions are made collaboratively, supported by data and strategy so the process feels intentional rather than reactive. With a dedicated partner managing the complexity, clients can stay focused on what matters most in their careers and lives without second-guessing every market move.